The world of finance can often seem like an exclusive club with its own language, filled with terms like derivatives, securitization, and amortization. While these concepts sound complex, many are built on simple, understandable ideas. One such term is “tranche.” At its core, a tranche is simply a slice or portion of a larger whole. By breaking down this concept, we can demystify a significant area of modern finance and empower you to better understand how financial markets operate.

This article will guide you through the essentials of tranches. We will explore what they are, how they function in financial products, and why they matter to investors and the broader economy.

What Exactly Is a Tranche?

The word “tranche” comes from the French word for “slice.” In finance, it refers to one of several related securities offered as part of the same financial deal. Imagine baking a large, multi-layered cake. While it is one cake, it has distinct layers, each with different ingredients or frosting. Some layers might be rich and dense, others light and airy. When you serve the cake, you cut it into slices, and each slice contains a piece of every layer.

Tranches work in a similar way. A financial institution might bundle together hundreds or thousands of individual loans—such as mortgages, auto loans, or credit card debt—into a single large pool. This pool of debt is then “sliced” into different segments, or tranches. Each tranche has its own set of rules, risks, and potential returns. Investors can then buy into the specific tranche that best matches their risk tolerance and investment goals.

These bundled loans are known as structured financial products, and tranches are the building blocks that make them work. The key takeaway is that not all tranches are created equal. They are specifically designed to have different levels of risk and reward, which allows them to appeal to a wide variety of investors.

A Brief History: The Rise of Securitization

The concept of tranches is closely tied to the development of “securitization,” a process that gained significant traction in the 1970s and 1980s. Securitization is the financial practice of pooling various types of debt—like mortgages—and selling them as bonds, or securities, to investors.

The first major use of this was in the mortgage market. Government-sponsored enterprises in the United States began buying individual home loans from banks and bundling them into what became known as mortgage-backed securities (MBS). This process had a dual benefit. It allowed banks to free up capital to issue more loans, and it gave investors a new way to invest in the real estate market without directly buying property.

Initially, these securities were simple. All investors in an MBS pool shared the risk and reward equally. However, financial engineers soon realized they could make these products more attractive by structuring them into tranches. By creating senior, mezzanine, and junior tranches, they could cater to different investor appetites. A pension fund seeking stable, low-risk returns could buy a senior tranche, while a hedge fund willing to take on more risk for a higher potential payout could purchase a junior tranche. This innovation dramatically expanded the market for structured financial products.

How Tranches Work in Practice: The Waterfall Effect

To understand how different tranches function, it’s helpful to visualize a waterfall. The money generated by the underlying assets (the monthly payments from mortgages, for example) flows into the structure like water at the top of a cascade. This cash flow then fills up a series of pools, one after another, from top to bottom.

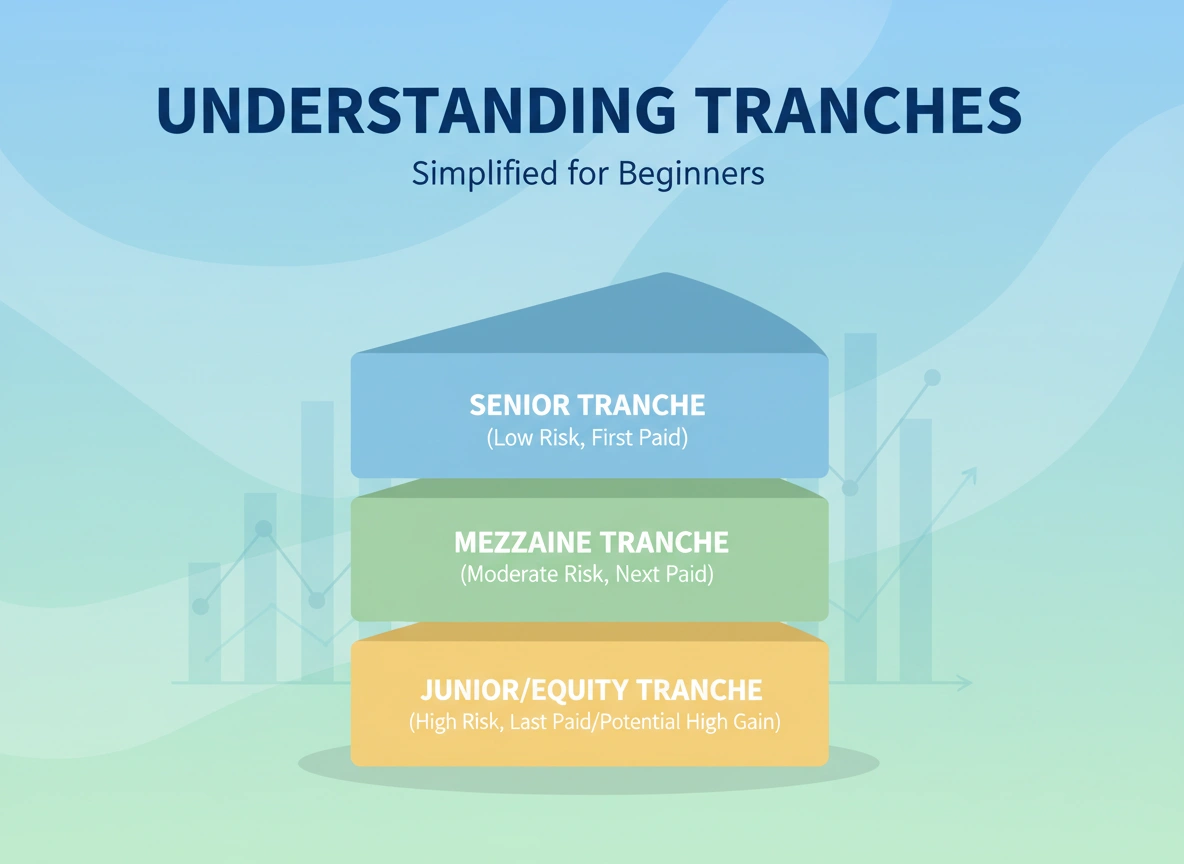

- Senior Tranches (The Top Pool): These are the highest-rated and least risky tranches. They are the first to receive payments from the underlying assets. Investors in senior tranches have priority and get paid before anyone else. Because of their safety, they typically offer the lowest interest rates or returns. These are often rated AAA, the highest credit rating available.

- Mezzanine Tranches (The Middle Pools): Situated below the senior tranches, mezzanine tranches absorb losses only after the junior tranches have been completely wiped out. They receive payments after the senior tranches are fully paid. To compensate for this increased risk, they offer higher returns than senior tranches. Their credit ratings are typically in the middle range, such as BBB.

- Junior Tranches (The Bottom Pool): Also known as the “equity” tranche, this is the riskiest segment. It is the first to absorb any losses from defaults in the underlying loan pool. For example, if some homeowners default on their mortgages, the junior tranche investors are the first to lose money. They are also the last to get paid. Because they take on the most risk, junior tranches offer the highest potential returns. These are often unrated or have a speculative-grade rating.

This payment priority system is what makes the entire structure work. It effectively concentrates risk in the lower tranches while protecting the higher ones, a process known as credit enhancement.

Risks and Benefits of Tranches

Tranches offer a sophisticated way to manage risk and return, but they come with their own set of advantages and disadvantages.

Benefits:

- Customization for Investors: The primary benefit is that tranches allow investors to choose a risk and reward profile that suits their specific needs. A conservative investor can stick to senior debt, while an aggressive one can seek higher yields in the junior tranches.

- Increased Liquidity: By pooling illiquid assets like individual loans and turning them into tradable securities, securitization increases liquidity in the market. This helps lenders free up their balance sheets to make new loans, stimulating economic activity.

- Diversification: For investors, buying into a tranched product can offer diversification. Instead of betting on a single loan, they are exposed to a large pool of loans, spreading out the risk of any single borrower defaulting.

Risks:

- Complexity and Lack of Transparency: Structured products are inherently complex. It can be difficult for investors to fully understand the quality of the thousands of underlying assets. The 2008 financial crisis famously highlighted this risk, as many securities backed by subprime mortgages were rated as safe senior tranches but were, in fact, extremely risky.

- Correlation Risk: The models used to create tranches assume that the underlying assets (e.g., mortgages) will not all default at the same time. However, in a widespread economic downturn, default rates can become highly correlated. When this happens, even senior tranches, once considered safe, can suffer significant losses.

- Valuation Challenges: Determining the true value of a tranche can be difficult, especially for the more complex structures. Their value depends on assumptions about future default rates, prepayment speeds, and recovery rates, all of which are hard to predict.

Practical Advice for Beginners

For someone new to finance, diving into tranched investments directly is not advisable. However, understanding the concept is crucial for grasping modern financial news and market behavior. Here are a few practical steps to build your knowledge:

- Start with the Basics: Before worrying about specific tranches, make sure you have a solid understanding of fundamental investment concepts like stocks, bonds, risk, and diversification.

- Follow the Financial News: Pay attention to how terms like “asset-backed securities” (ABS) or “collateralized debt obligations” (CDO) are used in financial reporting. Understanding the context will help solidify your knowledge.

- Read Reputable Sources: Seek out educational materials from established financial institutions, regulatory bodies, and reputable financial media. Focus on understanding the mechanics rather than chasing high-yield opportunities.

- Analyze the Underlying Assets: The quality of any tranched product depends entirely on the quality of the assets within it. The key lesson from history is to always question what is inside the package.

Conclusion

Tranches are a powerful financial tool that allows for the slicing and dicing of risk to meet the needs of different investors. By dividing a pool of assets into segments with varying levels of priority and risk, they create customized investment opportunities and add liquidity to the financial system. However, their complexity can obscure underlying risks, as demonstrated during the 2008 crisis.

For beginners, the goal is not to become an expert in structuring deals but to understand the principle: that large, complex financial products are often just collections of smaller, simpler pieces. By grasping the concept of a tranche as a “slice” with its own risk-return profile, you gain a clearer view of the structured finance landscape and become a more informed observer of the global economy.please click here for more info.

You may also read:Unique Dog Names to Strengthen Your Bond with Your Furry Friend

Leave a Reply